Mythbusting FAQs

Equity release is a big thing to consider and very different from your original mortgage. It is a way of releasing capital from your home without having to sell your property. It can also be a bit of a minefield. We believe in separating equity release fact from fiction, dispelling myths to give you a clear view of the path ahead.MYTH: EQUITY RELEASE IS LIKE A TRADITIONAL MORTGAGE

FACT: With a traditional mortgage, you purchase a home and make monthly payments which over time, reduces the amount you owe and builds up your ‘equity’. With a lifetime mortgage, the lender pays you a lump sum which is secured against your home and will be limited to a % of the property’s value. Typically, the older you are, the higher the % you can borrow. Lifetime mortgages typically don’t involve any monthly payments. The lump sum is paid out tax-free and the interest rate you pay back is fixed for life (variable rates are available too). The interest owed each month gets added to the balance and the loan (plus roll up interest) is paid back once the house is sold. Some products allow you to pay some or all of the interest either monthly or as-and-when. There is no end term with a lifetime mortgage; it is designed to run for the remainder of your life or until you need to go into care.

MYTH: I CAN’T TAKE OUT EQUITY RELEASE IF I STILL HAVE A MORTGAGE

FACT: Even if you have a mortgage, you can still take out equity release, but you’ll need to repay the mortgage from the released money first. Any money left over is yours to spend.

MYTH: AFTER I’VE GONE, MY CHILDREN WILL INHERIT A DEBT

FACT: You will never owe more than the value of your home. In fact, we only recommend plans with a ‘no negative equity guarantee’ approved by the Equity Release Council, so you can rest assured that your children will not inherit any debt.

MYTH: I WON’T OWN MY HOME

FACT: With a Lifetime Mortgage, you will still own 100

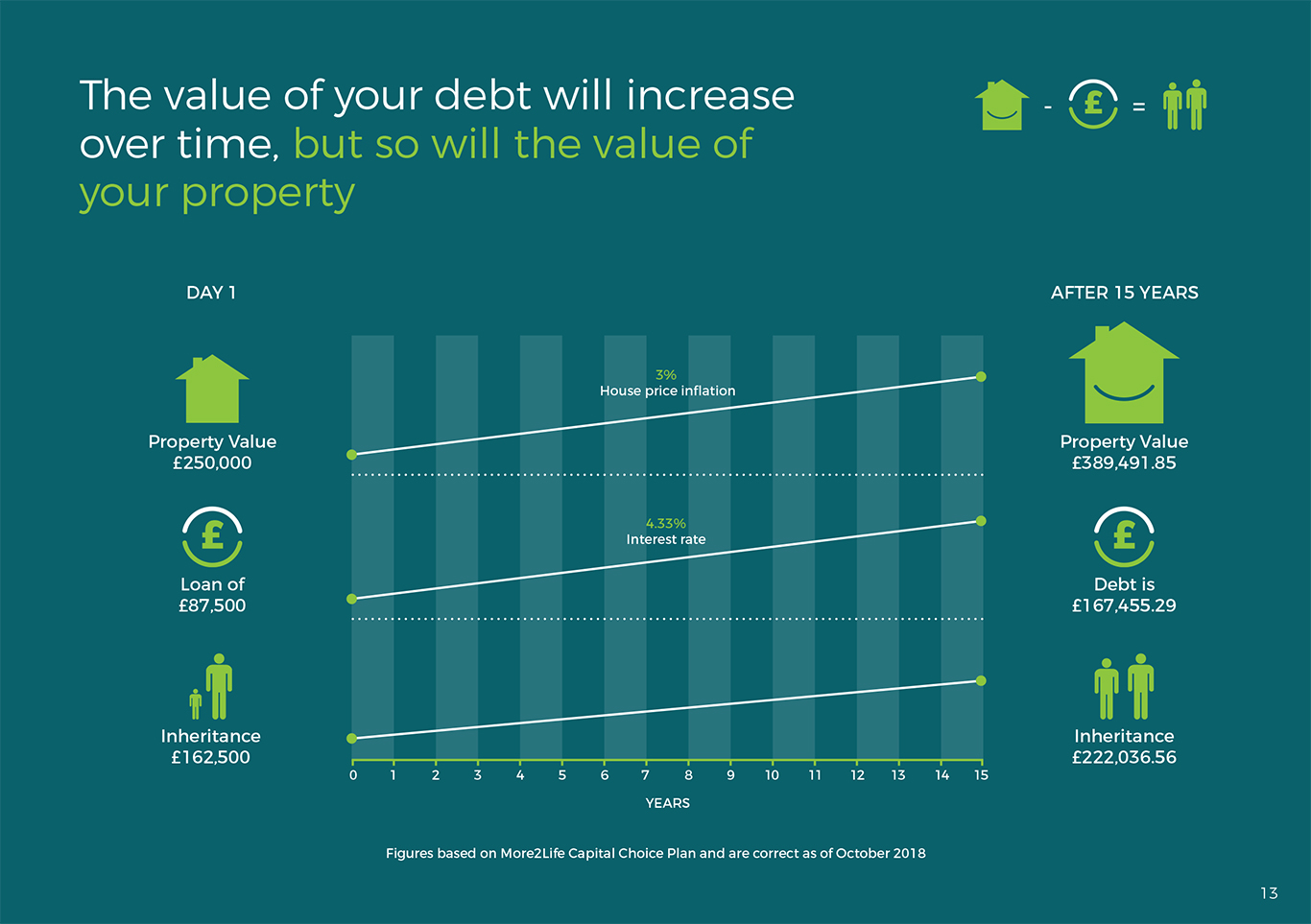

MYTH: THERE WILL BE NO INHERITANCE LEFT FOR MY CHILDREN

FACT: Taking out equity release is a great way of helping you to enjoy the retirement you deserve and to help your family while you are still living. Equity release will reduce the value of your estate as you will be accruing interest on the loan, but don’t forget that your property’s value

MYTH: HAVING EQUITY RELEASE WILL AFFECT MY BENEFITS

FACT: The good news is that the cash released is tax-free. However, it may affect your entitlement to some state benefits as your wealth may significantly increase as a result of taking out equity release. Before you go ahead, we will help you determine how equity release will affect any benefits you receive. You may even find you are entitled to some additional benefits not yet considered.

Contact us for your free, no obligation quote returned within 24 hours.

Don’t let retirement pass you by.

Let us help you have the retirement you deserve.

01603 85 85 80

Call us today for your free, no obligation quote